With rising pressure from governments, investors, and consumers to address climate change, businesses are increasingly expected to manage and disclose their company’s carbon footprint. Carbon accounting, also called greenhouse gas accounting, has become a prerequisite for companies looking to reduce their environmental impact, enhance their sustainability credentials, and comply with regulatory requirements. Tracking and reporting emissions is now essential for any business serious about contributing to global efforts to combat climate change.

As of 2025, 92% of global GDP has made an intended or actual commitment to reaching net zero by 2050, driving the demand for robust greenhouse gas (GHG) accounting to demonstrate commitment to decarbonization. Governments worldwide are implementing mandatory reporting laws, such as the EU’s Corporate Sustainability Reporting Directive (CSRD) and California’s SB 253, which necessitate accurate carbon accounting to avoid fines and legal issues.

In this blog post, we’ll explore what carbon accounting entails, explain the different carbon accounting methods available, and guide you in selecting the best approach for your business. Understanding these methods will help your organization make informed decisions on reducing carbon emissions across your value chain and enable accurate carbon accounting and reporting to stakeholders.

What is carbon accounting?

The foundation of greenhouse gas emissions measurement

Carbon accounting, also known as greenhouse gas accounting, is a framework of methods to measure and track how much greenhouse gas (GHG) an organization emits, helping to limit climate change. At its core, corporate carbon accounting is the process of measuring, quantifying, and reporting the greenhouse gas emissions associated with a company’s operations. These emissions are often calculated in carbon dioxide equivalents (CO2e) to account for all GHGs, including methane and nitrous oxide, which have a greater warming potential than carbon dioxide.

Carbon accounting enables businesses to better understand their environmental impact and take concrete actions to reduce emissions, improve operational efficiency, and meet regulatory requirements or voluntary sustainability goals. As climate regulations tighten and investor scrutiny increases, carbon accounting has become essential for businesses that want to remain competitive and credible in the market.

The carbon accounting process

The carbon accounting process typically involves collecting emissions data from a variety of sources, such as energy usage, transportation, production processes, and purchased goods and services. This sustainability data is then used to calculate the total GHG emissions across different scopes, defined by the Greenhouse Gas Protocol as Scopes 1, 2, and 3.

Carbon accounting requires comprehensive data collection and processing methodologies to accurately estimate an organization’s carbon footprint, which is essential for setting reduction targets and tracking progress. The data quality of your emissions calculations directly affects the reliability of your carbon reporting and your ability to achieve net zero emissions targets.

Understanding the three scopes of greenhouse gas emissions

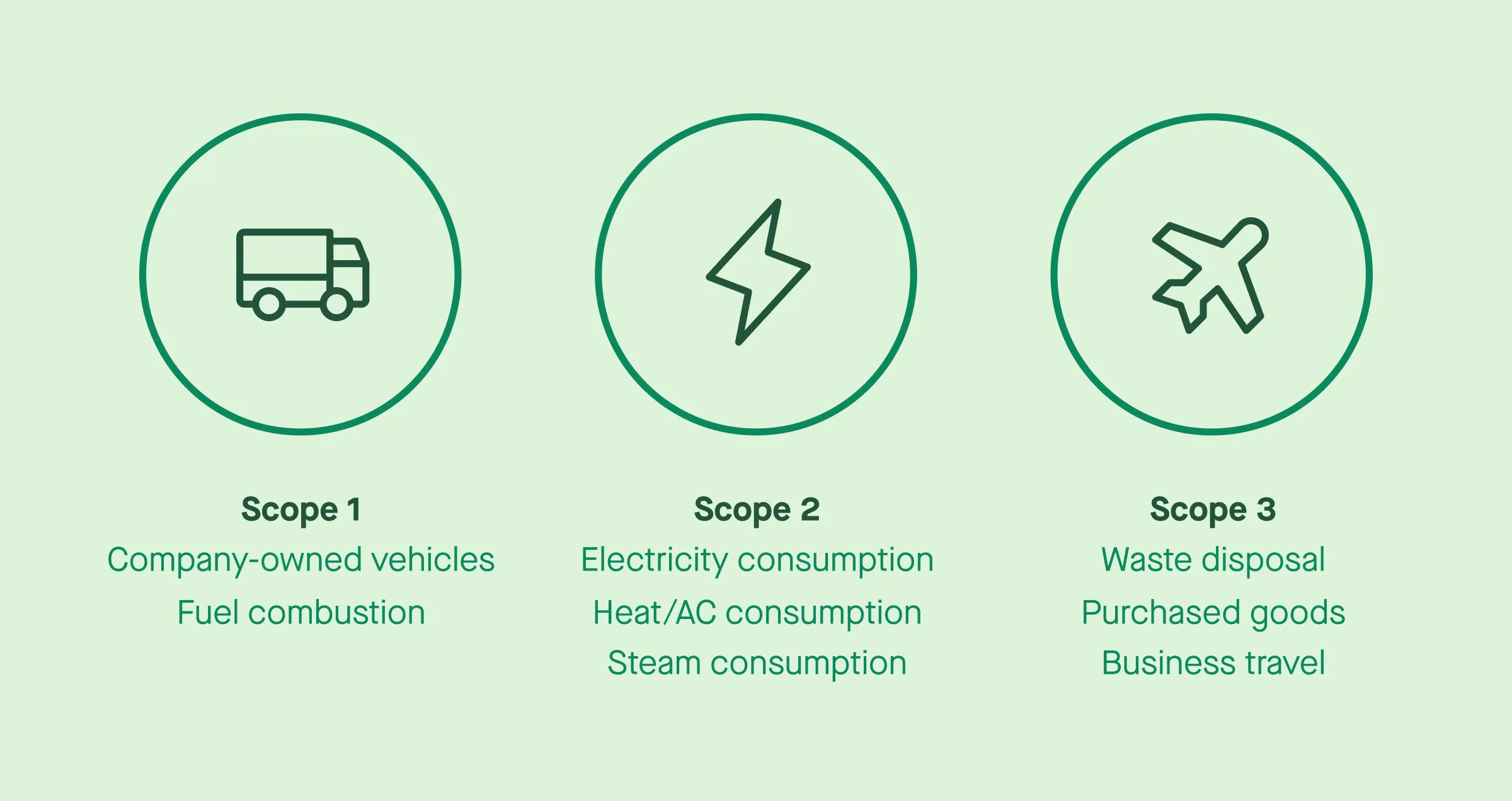

Under the Greenhouse Gas Protocol, emissions are classified into three scopes: Scope 1, Scope 2, and Scope 3, which help organizations categorize their greenhouse gas emissions based on their source. The Greenhouse Gas Protocol is the most widely used standard for carbon accounting, developed by the World Resources Institute and the World Business Council for Sustainable Development.

Scope 1: Direct emissions

Scope 1 emissions are direct greenhouse gas emissions that occur from sources owned or controlled by an organization, such as emissions from company vehicles and manufacturing processes. Scope 1 includes direct emissions that occur from sources owned or controlled by a company. These emissions come from activities like fuel combustion in company-owned vehicles, boilers, and furnaces, as well as emissions from on-site industrial processes and burning fossil fuels.

Scope 1 emissions are within a company’s direct control, meaning that reducing these emissions can be achieved through actions like improving energy efficiency, switching to cleaner fuels, or adopting electric vehicles. Common sources include natural gas combustion for heating, diesel fuel for fleet vehicles, and process emissions from manufacturing facilities.

Scope 2: Indirect emissions from purchased energy

Scope 2 emissions are indirect greenhouse gas emissions from the consumption of purchased electricity, steam, heating, and cooling, which are necessary for an organization’s operations. Scope 2 encompasses indirect emissions from the generation of purchased electricity, heat, or steam that a company consumes. While the company does not directly produce these emissions, they are caused by its energy consumption.

Reducing Scope 2 emissions typically involves switching to renewable energy sources, increasing energy efficiency, or purchasing renewable energy certificates to offset the emissions from purchased electricity. Companies can also work with utilities to source cleaner energy or install on-site renewable generation like solar panels.

Scope 3: Indirect emissions across the value chain

Scope 3 emissions encompass all other indirect emissions that occur in a company’s value chain, including those from suppliers and the use of sold products, and often represent the largest portion of a company’s total emissions. The Greenhouse Gas Protocol emphasizes that Scope 3 emissions can be significantly larger than Scope 1 and Scope 2 emissions, highlighting the importance of engaging suppliers to reduce these emissions.

Scope 3 often represents the largest source of corporate greenhouse gas emissions, accounting for an average of 5.5 times more emissions than a company’s direct emissions. This includes emissions from suppliers, the transportation of goods, employee commuting, business travel, and even the use and disposal of products.

Scope 3 is also the hardest to measure and control, as it depends on external partners and requires data collection across your entire value chain. Reporting and reducing Scope 3 emissions is particularly relevant for organizations that report to the Carbon Disclosure Project (CDP) or have committed to the Science Based Targets initiative (SBTi). Engaging suppliers to report and reduce Scope 3 emissions can yield significant reductions in overall emissions, as these emissions are often linked to the activities of numerous organizations in the supply chain.

By accurately measuring carbon emissions across these scopes, companies can gain a clear understanding of their business’s carbon footprint and make informed decisions about how to reduce their climate impact. However, choosing the right carbon accounting methodology is critical to ensuring that accurate emissions data is consistent and actionable.

Different carbon accounting methods

There are several carbon accounting methods that businesses can use to measure carbon emissions. These methods vary based on the type and quality of data available and the level of detail required. The most common methods include the spend-based method, activity-based method, and hybrid method. Each has its own unique approach to calculating emissions, as outlined below.

Spend-based method

The spend-based method is one of the simplest approaches to carbon accounting. This method estimates emissions based on financial data and spending records. It involves multiplying the amount spent on a particular good or service by an emission factor associated with that category of expenditure.

For example, a company might estimate its emissions from business travel by analyzing the total amount spent on flights, hotels, and transportation. The spend-based method applies predefined emission factors to these financial accounting amounts to estimate the associated greenhouse gas emissions. These emission factors are typically derived from general industry averages or published databases like the Environmental Protection Agency, reflecting average emissions for similar types of spending.

This method is particularly useful for businesses at the beginning stages of their carbon accounting journey or for those lacking detailed activity data. It offers a straightforward way to get an initial estimate of emissions based on financial records that are already maintained.

Advantages:

- Simplicity: The spend-based method is straightforward and easy to implement because it relies on financial data that businesses already track.

- Ease of Implementation: Businesses can quickly apply emission factors to financial data to estimate emissions without needing extensive additional manual data collection.

Disadvantages:

- Rough Estimates: This method can provide only approximate estimates of emissions, as it assumes all spending within a category results in the same level of emissions. Variations between suppliers or products are not accounted for.

- Lack of Precision: For instance, a $1,000 expenditure on flights with different airlines might result in varying emissions due to differences in flight routes, aircraft efficiency, and carrier practices, which the spend-based method cannot capture.

Activity-based method

The activity-based method offers a more detailed approach to measuring carbon emissions by using specific activity data rather than financial expenditures. This method involves tracking actual activities, such as the amount of electricity used, miles traveled by vehicle, or volume of raw materials consumed. Each of these activities is then multiplied by corresponding emission factors to calculate total emissions.

For example, a company might track the number of kilowatt-hours of electricity consumed in its manufacturing processes. The emissions are calculated using an emission factor specific to the electricity grid in the region where the factory operates. Similarly, transportation emissions can be calculated by tracking miles traveled by delivery vehicles and applying emission factors for fuel combustion.

This method provides a more precise estimate of emissions because it is based on actual usage data and calculating emissions from real activities. However, it requires more detailed record-keeping and a greater commitment of resources to gather and manage the necessary sustainability data.

Advantages:

- Higher Accuracy: The activity-based method yields more accurate emissions data because it uses specific data on actual activities rather than financial proxies.

- Reflects Actual Usage: It provides a more detailed and precise picture of how much greenhouse gas your operations produce by accounting for the actual usage of resources and activities.

Disadvantages:

- Data Collection Effort: Requires detailed record-keeping and the allocation of resources to collect and manage activity data, which can be labor-intensive.

- Complexity: Tracking and applying the appropriate emission factors for various activities can be complex and demanding, particularly for Scope 3 emissions across the supply chain.

Hybrid method

The hybrid method combines elements of both the spend-based and activity-based approaches. This method is particularly useful for businesses with complex operations or those transitioning toward more detailed carbon accounting practices. The hybrid method allows companies to use spend-based calculations where detailed activity data is not yet available and switch to activity-based calculations for areas where specific data can be collected.

For example, a company might use the spend-based method to estimate emissions from office supplies or professional services. For more precise measurements, such as emissions from electricity use or manufacturing processes, the company could apply the activity-based method. This blend of approaches enables businesses to balance accuracy with practicality while improving data quality over time.

Advantages:

- Balanced Approach: Combines the simplicity of spend-based calculations with the accuracy of activity-based methods, providing a flexible solution for different types of emissions data.

- Flexibility: Allows businesses to start with simpler methods and gradually transition to more detailed calculations as more data becomes available across their value chain.

Disadvantages:

- Complexity in Integration: Combining two methods can introduce challenges in integrating and interpreting carbon data from both approaches.

- Transition Challenges: Moving from spend-based to activity-based data may present difficulties in aligning and reconciling different types of emissions calculations.

In summary, each carbon accounting method has its own strengths and limitations. Choosing the right method, or a combination of methods, depends on the specific needs of your business, the available emissions data, and the level of detail required for accurate carbon reporting.

How to choose the best carbon accounting method for your business

Choosing the right carbon accounting method for your business depends on a variety of factors, including the complexity of your operations, the availability of data, and the level of detail you want to achieve in your emissions tracking. To determine the best approach, consider the following factors:

Data availability

Start by assessing the type and quality of data your company can access. If detailed activity data is readily available, such as records of energy consumption, travel distances, or material usage, then an activity-based or hybrid approach might be best. On the other hand, if your sustainability data is more limited or fragmented, starting with a spend-based method could provide a reasonable first step toward accurate carbon accounting.

Business complexity

The complexity of your business will also play a key role in choosing the appropriate carbon accounting methodology. For small businesses with straightforward operations, the spend-based method may offer a practical solution. For larger organizations with more diverse and complex value chains, an activity-based or hybrid approach can deliver more granular insights and help identify specific areas for reducing carbon emissions.

Resource availability

Carbon accounting and emissions reporting require a commitment of time, effort, and financial resources. Companies with limited resources may find it more practical to begin with spend-based carbon accounting methodologies before investing in the more data-intensive activity-based approach. The hybrid method can offer a scalable option, allowing businesses to enhance the accuracy of their carbon metrics over time without overwhelming their resources.

Goals and regulations

Your sustainability goals and regulatory requirements should guide your choice of a carbon accounting method. The EU’s Corporate Sustainability Reporting Directive (CSRD) requires many large companies to disclose a broad array of ESG information, including greenhouse gas emissions, as part of its goal to make EU countries carbon neutral by 2050.

In 2022, the US Securities and Exchange Commission (SEC) proposed a rule requiring all public companies to report Scope 1 and Scope 2 emissions, with larger companies required to disclose Scope 3 emissions if they are material or if the company has set an emissions target that includes Scope 3.

If your company is required to meet specific emissions reduction targets or comply with climate-related regulations like California SB 253, you may need a more detailed approach to ensure your emissions data is accurate and transparent. Similarly, if you are aiming to achieve ambitious sustainability goals, such as net zero emissions, a hybrid or activity-based approach will provide the level of detail needed to track progress and make informed decisions.

Evolving accuracy in carbon accounting

Annual carbon accounting is an evolving process. While businesses may start with simpler methods, such as the spend-based approach, they can progressively refine their carbon accounting methodologies as they gather more specific emissions data over time. This gradual improvement in accuracy can help organizations move from basic emissions estimates to more precise company’s carbon emissions measurements.

For example, a company might initially use a spend-based method to estimate emissions from its suppliers, but as it begins to engage more deeply with its value chain, it could collect activity-based data on energy consumption, raw materials usage, and transportation practices. Over time, the carbon accounting process becomes more robust, allowing for more accurate measurement of greenhouse gas emissions across the entire operation.

This iterative approach is particularly useful for companies just beginning their carbon accounting journey. By starting with rough estimates and gradually building a more detailed emissions inventory, businesses can take meaningful steps toward carbon reduction while continuing to improve their understanding of their environmental impact. As data availability increases and emission factors are better understood, carbon accounting can evolve into a more precise tool for driving sustainable development.

Companies that implement carbon accounting can discover unexpected business benefits, including minimizing risk, building brand equity, and reducing inefficiency. Accurate emissions data from carbon accounting enables organizations to identify inefficiencies in their operations, leading to cost savings and improved performance.

How can carbon accounting software help?

Carbon accounting software platforms have become essential tools in helping businesses accurately measure and manage their greenhouse gas emissions. These platforms automate the carbon accounting process, making it more efficient and accurate. Here’s how they can help:

Automating the collection of emissions data

One of the most significant advantages of carbon accounting platforms is their ability to automate data collection. Instead of relying on manual data collection processes or broad estimates, these platforms gather precise emissions data from various sources. For example, they can collect activity data from suppliers, partners, and other parts of the value chain, leading to more accurate and specific emissions calculations. This granular data improves the accuracy of carbon dioxide equivalents calculations and allows businesses to make informed decisions about their carbon reduction strategies.

Refining emissions estimates with better data

Carbon accounting software also supports a transition from spend-based calculations to more refined activity-based methods as businesses gather more detailed data over time. Initially, many companies may start with high-level estimates, but as more specific data becomes available from suppliers and internal operations, these platforms allow businesses to shift toward more precise GHG accounting methods. This evolution in accuracy helps companies stay current with their carbon accounting methodologies and ensures they can measure emissions produced more effectively as their processes mature.

Enhancing emissions reporting and compliance

Another key feature of carbon accounting platforms is their ability to simplify carbon reporting. Many platforms are designed to align with recognized standards, such as the Greenhouse Gas Protocol or the Science Based Targets initiative (SBTi). Automated reporting capabilities make it easier for businesses to comply with regulatory requirements and share progress transparently with stakeholders. This functionality helps ensure that companies remain accountable in their efforts to reduce emissions while building trust with investors, customers, and regulators.

The platforms also support reporting to frameworks like the Carbon Disclosure Project (CDP), Sustainability Accounting Standards Board (SASB), and ESG ratings calculation process, helping companies maintain credibility in the market.

Driving more effective emission reductions

By improving data quality and reporting capabilities, carbon accounting software empowers businesses to take more effective actions toward reducing carbon emissions. With a clearer understanding of their company’s carbon footprint, companies can identify key areas where emission reductions can be made, whether it’s within their operations, supply chain, or through carbon offsets strategies. This level of insight is crucial for setting and achieving meaningful net zero targets.

Companies with robust carbon accounting may secure better lending terms or access to green investment funds, as investors assess long-term financial risk based on carbon data. The financial benefits extend beyond operational efficiency to include improved access to capital and enhanced reputation.

How do you choose the right carbon accounting platform for your business?

Selecting the right carbon accounting software for your business is a critical step in effectively managing your greenhouse gas emissions. With a wide variety of platforms available, it’s important to choose one that aligns with your specific needs and goals. Here are key factors to consider when making your decision:

Assess your business needs and scope

The first step in choosing the right platform is to assess your business’s carbon accounting needs. Consider the scope of emissions you need to track, whether it’s Scope 1 (direct emissions from fossil fuels and fuel combustion), Scope 2 (indirect emissions from purchased electricity), or Scope 3 (indirect greenhouse gas emissions from your value chain). Businesses with complex supply chains or operations across multiple regions may require more sophisticated platforms that can handle a broader range of emissions tracking, whereas smaller companies with simpler operations may need a more straightforward solution.

Data integration and accuracy

Another important factor is the platform’s ability to integrate with your existing systems and accurately capture accurate emissions data. Look for platforms that can easily integrate with your internal tools, such as energy monitoring systems, financial software, or procurement platforms. Additionally, the platform should be able to pull in data from external sources, such as suppliers and partners, which is particularly important for Scope 3 emissions tracking. This ability to gather granular activity data across your value chain will help improve the accuracy of your carbon accounting process over time.

Flexibility and scalability

Your carbon accounting needs may evolve as your business grows or as regulatory requirements change. Choose a platform that is flexible and scalable to accommodate changes in your carbon accounting methodologies. For example, some businesses might start with spend-based calculations but eventually transition to activity-based or hybrid methods as they collect more precise data. The right platform should support this progression and allow you to refine your emissions calculations over time.

Compliance and reporting capabilities

Make sure the platform you choose supports compliance with key reporting standards and frameworks, such as the GHG Protocol, the Science Based Targets initiative (SBTi), or regional regulatory requirements like California SB 253 and the CSRD. The platform should offer automated reporting features that allow you to generate reports for both internal use and external stakeholders. Strong sustainability reporting capabilities not only help you stay compliant but also enable transparent communication of your progress in reducing emissions.

Ease of use and support

Usability is a crucial consideration when selecting a carbon accounting platform. Ensure the platform is user-friendly and provides adequate training and support. An intuitive interface can save time and reduce the learning curve for your team, allowing them to focus on interpreting the carbon data and taking action. Additionally, strong customer support, either through online resources or direct assistance, can be invaluable when navigating complex carbon accounting challenges.

Cost and return on investment

Finally, consider the cost of the platform in relation to the value it will provide for your business. While some platforms may require a larger initial investment, they may offer greater accuracy, integration capabilities, and long-term scalability.

It’s important to weigh the benefits of a more sophisticated platform against the upfront cost to ensure it aligns with your sustainability goals and business objectives. Choosing the right platform is an investment in your company’s ability to effectively measure, report, and reduce greenhouse gas emissions, which can drive significant returns in the form of operational efficiency, regulatory compliance, and enhanced reputation.

The importance of accuracy and adaptability in carbon accounting

Why is carbon accounting important? The carbon accounting process is critical for any business aiming to reduce its carbon footprint and contribute to the fight against climate change. By employing diverse carbon accounting methods, companies can get a detailed insight into their company’s carbon emissions. Whether you choose to begin with a spend-based approach or dive into more detailed activity-based calculations, the key is to ensure that your carbon accounting methodology evolves alongside your data availability and business needs.

By embracing a flexible, iterative approach to measuring greenhouse gas emissions, businesses can develop more accurate and actionable insights over time, positioning themselves for long-term success in sustainability. As climate regulations tighten and investor scrutiny increases, carbon accounting has become essential for businesses that want to remain competitive and credible in the market.

Carbon accounting is not a static exercise. It’s an ongoing process that enables companies to refine their emissions data and methodologies as they grow and learn. As the accuracy of carbon calculations improves through better emission factors and data collection, so too does the ability to reduce emissions and mitigate the impacts of climate change, paving the way for achieving net zero and contributing to sustainable development.

Understanding residual emissions, those remaining after all feasible emission reductions have been made, is also critical for companies pursuing net zero targets. These residual emissions may need to be addressed through high-quality carbon offsets or other mechanisms to achieve true carbon neutrality.