Update as of Feb 26: The new Omnibus has been announced – Read our thorough update here.

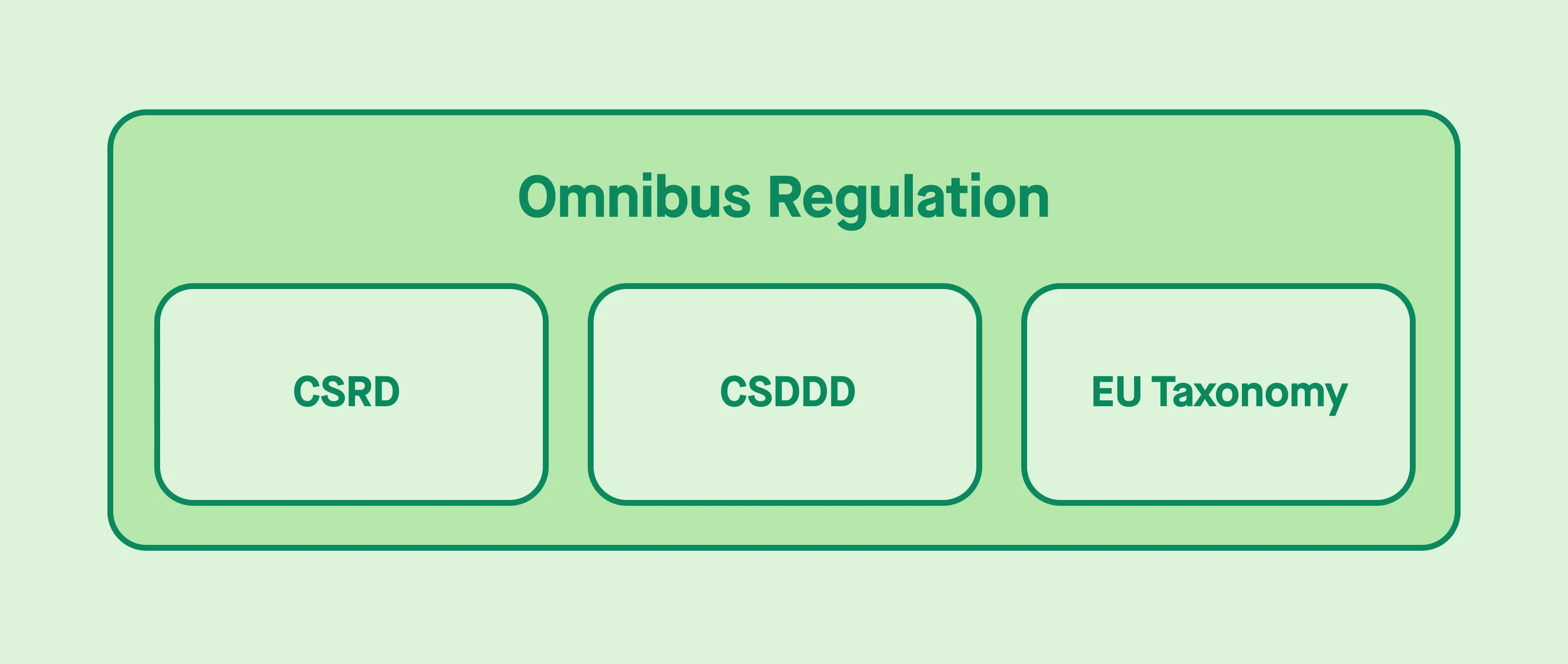

The European Union’s Omnibus legislation promises to reshape the corporate reporting landscape by consolidating multiple sustainability-related requirements into a single, streamlined framework. Announced by European Commission President Ursula von der Leyen in November 2024, the regulation aims to simplify the often-overlapping obligations under the Corporate Sustainability Reporting Directive (CSRD), Corporate Sustainability Due Diligence Directive (CSDDD), and the EU Taxonomy Regulation. The Omnibus Regulation, scheduled for publication in 2025, is designed to reduce bureaucracy without compromising on content, ensuring businesses operating in EU member states can focus on compliance while driving sustainability.

This article unpacks what we know so far about the Omnibus Regulation, the regulatory backdrop, and the critical role of organizations like EFRAG in shaping its implementation. We’ll update this piece regularly as new information emerges.

What has been mentioned about the Omnibus Regulation so far?

President von der Leyen’s announcement highlighted the need to reduce the administrative burden for companies while maintaining the high standards expected under existing ESG frameworks. The new regulation aligns with the EU’s broader competitiveness agenda, as outlined in the Budapest Declaration and other strategic documents.

Key elements of the Omnibus Regulation include:

- Consolidating the CSRD, CSDDD, and EU Taxonomy Regulation.

- Reducing reporting requirements by 25% while preserving the substantive elements of the frameworks.

- Promoting consistency across Member States to ensure fair and effective compliance.

The regulation is part of the EU’s broader effort to streamline its legislative environment and enhance competitiveness, as outlined in the July 2024 Political Guidelines for the Next European Commission.

What is the Budapest Declaration?

The Budapest Declaration on the New European Competitiveness Deal is a 12-point plan aimed at fostering economic prosperity, resilience, and security. Adopted after a meeting of EU leaders and senior European Commission representatives in Budapest, the declaration underscores the need for regulatory simplification in order to boost competitiveness.

A key aspect of the declaration is its call for a “simplification revolution,” which includes a target to reduce reporting requirements by 25% by mid-2025. While the goal is ambitious, von der Leyen has clarified that simplification will focus on reducing overlaps rather than trimming substantive obligations.

The Budapest Declaration reflects a balancing act between maintaining high ESG standards and enabling European companies to navigate the complex regulatory environment with greater ease.

Which regulations might the Omnibus Directive combine?

The Omnibus Directive will integrate three cornerstone ESG regulations, each of which plays a critical role in the EU’s sustainability agenda:

Corporate Sustainability Reporting Directive (CSRD)

The CSRD expands sustainability reporting requirements to cover a broad range of environmental, social, and governance (ESG) issues. Starting in 2025, it applies to large companies and listed SMEs, requiring detailed disclosures on sustainability impacts, risks, and strategies. The directive aims to enhance transparency and comparability across businesses, providing investors and stakeholders with consistent, reliable data.

Corporate Sustainability Due Diligence Directive (CSDDD)

The CSDDD emphasizes corporate accountability, requiring companies to identify, mitigate, and address human rights and environmental risks throughout their value chains. It’s a pivotal regulation for fostering ethical practices and ensuring supply chain transparency. Businesses must adopt comprehensive due diligence processes and engage actively with stakeholders to meet these obligations.

EU Taxonomy

Designed as a classification tool, the Taxonomy Regulation defines which economic activities qualify as environmentally sustainable. It guides businesses and investors toward green initiatives, supporting the EU’s climate neutrality goals. The taxonomy also enhances transparency by standardizing definitions and criteria for sustainable activities, reducing the risk of greenwashing.

Together, these regulations form the backbone of the EU’s ESG reporting framework. Their integration under the Omnibus Directive represents a significant step toward simplifying compliance while maintaining rigor.

What is EFRAG and what role has it played?

The European Financial Reporting Advisory Group (EFRAG) has been instrumental in shaping the EU’s sustainability reporting landscape. Its role extends beyond technical guidance, focusing on facilitating the adoption and implementation of robust reporting standards.

Clarifying complexities in reporting:

EFRAG has addressed widespread misconceptions about sustainability reporting by emphasizing that regulations like the CSRD were introduced in response to market demand for more granular and comparable data. For example, EFRAG’s Implementation Guidance (IG) 3 includes nearly 800 data points to improve reporting accuracy, though some have decried a lack of clear prioritization.

Supporting SMEs:

Recognizing the unique challenges faced by SMEs, EFRAG introduced voluntary sustainability reporting standards tailored for smaller businesses in December 2024. These standards aim to ease the learning curve for SMEs and promote gradual adoption of what will one day become mandatory requirements.

Driving global alignment:

EFRAG works closely with international bodies like the ISSB to harmonize sustainability standards. This includes advancing interoperability between EU regulations and global frameworks, ensuring consistent reporting practices across jurisdictions.

Innovating through technology:

EFRAG advocates for the integration of AI and digital tools in reporting processes. Digital taxonomies, for example, can enhance efficiency and reduce the administrative burden on businesses, allowing them to focus on delivering meaningful disclosures.

Looking ahead:

As the EU prepares for sector-specific standards, EFRAG emphasizes the importance of materiality assessments to tailor disclosures to industry-specific risks and opportunities. It also highlights the need for early stakeholder engagement to align EU and international standards effectively.